Ways to Optimize Financial Planning Online Without Costly Mistakes

Welcome to the cold, bright reality of digital finance—a world where a thousand apps want your attention, algorithms whisper sweet nothings about your future, and every click feels like a leap of faith. The idea of optimizing financial planning online is seductive: tap a few buttons, automate your path to wealth, and bask in the glow of a dashboard that promises control. But for most, the results are less “master of your destiny” and more “lost in a maze of logins, fees, and broken promises.” This isn’t the feel-good story you’ve read before. This is a deep dive into the hard truths, hidden traps, and smarter moves for turning digital chaos into real financial power. If you’re tired of the hype and ready for the edge, let’s tear off the digital mask and see what really works when optimizing your finances online—armed with research, unfiltered stories, and sharp-eyed skepticism. Your financial future doesn’t start tomorrow; it starts the moment you see through the noise.

Why financial planning online is broken—and how to fix it

The digital revolution nobody asked for

The shift from paper ledgers and in-person meetings to digital dashboards was less a revolution by demand and more an inevitability forced by convenience, cost-cutting, and the relentless march of tech. In the late 2010s, financial institutions scrambled to roll out apps, platforms, and “robo-advisors” in a bid to capture mobile-first consumers. COVID-19 only accelerated the exodus from brick-and-mortar. Suddenly, everyone—from retirees to side hustlers—was thrust into a world where financial planning was one browser tab among many.

Promise was high: democratized access, lower fees, and the ability to manage everything from asset allocation to grocery budgets without ever shaking a banker’s hand. But reality hit hard fast. Too many tools, too little guidance, and a sense that, while friction was gone, so was the personal touch. According to a 2025 Moneywise study, 35% of U.S. adults expect to be better off financially in four years, but most report confusion and overwhelm with digital options. The revolution delivered access, but at the cost of clarity.

The paradox of choice: overwhelmed by options

For anyone staring down a grid of apps in the App Store, the explosion of online financial planning tools is dizzying. With more than 500 digital finance products on the U.S. market in 2025, the average consumer faces a paradox: more choice, but less certainty. Sorting between platforms promising AI-powered advice, bank-grade security, and one-click tax optimization turns financial planning into decision fatigue.

| Platform | Usability | AI Features | Data Security | Pricing | User Satisfaction |

|---|---|---|---|---|---|

| Betterment | High | Advanced | Excellent | $$ | 4.5/5 |

| Mint | Medium | Limited | Good | Free | 4.1/5 |

| Abacum | High | Moderate | Excellent | $$$ | 4.2/5 |

| Personal Capital | Medium | Good | Excellent | $$ | 4.3/5 |

| YNAB | High | None | Good | $$$ | 4.7/5 |

Table: Top 5 online financial planning platforms in 2025. Source: Original analysis based on Abacum, Moneywise, Financial Planning

But here’s the kicker: more isn’t always better. According to academic research on decision-making, excessive choice leads to anxiety and, ironically, worse outcomes (Financial Planning, 2025). Many users bounce between apps, never sticking long enough to benefit from compound insights or habit formation. It’s a digital buffet where the abundance leaves you hungry.

The hidden costs of going digital

Behind the frictionless dashboards and slick onboarding, online financial planning carries costs few talk about. Subscription creep is real: multiple $5-$50 monthly fees for budgeting, investing, and tax optimization silently eat into savings. Then there’s the matter of algorithmic bias—AI models trained on incomplete data may push you into cookie-cutter strategies that don’t fit your life.

Less obvious, but far more sinister, are the data vulnerabilities. Convenience comes at the price of sharing intimate financial details with third parties. As one recent user, Riley, put it:

"People think tech equals safe. But convenience always comes at a price." — Riley (illustrative, based on user sentiment studies)

The reality: trust misplaced in an app or algorithm can have lasting consequences. Poor advice is just as scalable as good advice online, and when things go wrong, customer support is often a chatbot deep in a foreign call center. The long-term implication? A generation growing up thinking finance is “set and forget,” blind to the ways unchecked automation and opaque algorithms can unravel even the savviest plan.

Debunking the biggest myths of online financial optimization

Myth #1: All online tools are basically the same

It’s tempting to believe every budgeting app or robo-advisor is a variant of the same solution. The truth? The landscape stretches from static spreadsheets to bleeding-edge AI that predicts cashflow and tax liabilities in real time. Some platforms focus on simple expense tracking, others on portfolio management, and a select few offer integrated planning across business and personal lines.

- Hidden benefits of online financial planning experts won’t tell you:

- Real-time data aggregation exposes blind spots in spending and investment.

- AI-driven insights can flag hidden fees or underperforming assets faster than human advisors.

- Automated tax-loss harvesting optimizes after-tax returns, a feature rarely available offline.

- Fractional investing gives access to assets (like commercial real estate or start-ups) previously reserved for the ultra-wealthy.

- Transparent dashboards improve advice recall—a known weakness in traditional planning (Financial Planning, 2025).

- Regular software updates mean strategies adapt in real-time to regulatory changes or market shocks.

- Integrated charitable giving tools make tax-optimized philanthropy as simple as a swipe.

Pick the wrong tool, though, and you’re not just missing features—you’re risking misaligned priorities, security holes, and wasted time. Choosing based on hype over fit can derail your progress fast.

Myth #2: DIY online planning is only for the young and tech-savvy

Forget the stereotype of the hoodie-wearing millennial automating their way to wealth. Thanks to improved accessibility, more intuitive design, and better onboarding, online financial planning is now a cross-generational game. According to Moneywise (2025), 45% of 18–29-year-olds are optimistic about their financial future, but late adopters—retirees, parents, small business owners—are closing the gap.

Take the story of Marlene, a 67-year-old who, after years of ignored bank statements, started using Mint with her granddaughter’s help. Within months, she’d flagged duplicate subscriptions, set up automated bill pay, and even began investing small amounts in diversified ETFs. The lesson? Good design and guided onboarding break down barriers once thought insurmountable.

Myth #3: Digital tools make financial mistakes impossible

Automation is a double-edged sword. When set up right, it minimizes human error and emotional overreaction. But a misconfigured rule—say, an aggressive auto-investment or a faulty recurring transfer—can turn a helpful tool into a disaster engine.

"AI is only as smart as the joker using it." — Jordan (illustrative, based on expert consensus)

Critical thinking—questioning recommendations, checking underlying assumptions, and understanding tool limitations—remains non-negotiable. Blind trust in “smart” apps has caused more than one user to overdraft, misallocate funds, or trigger unintentional tax liabilities. The best digital platforms empower users to review, question, and adjust—not abdicate responsibility.

Step-by-step: How to actually optimize your finances online

Assess your real needs before you click

Digital optimization starts long before you download an app or sync a bank account. Without self-assessment, even the best technology is just noise. Ask: What am I really trying to achieve? Is it debt reduction, investment growth, expense tracking, or something more nuanced?

- Priority checklist for digital financial planning readiness:

- List all sources of income and expenses.

- Identify financial goals (short, medium, long-term).

- Assess existing online accounts and tools.

- Evaluate comfort level with technology and automation.

- Set up two-factor authentication for all sensitive accounts.

- Research at least three tools for each financial need.

- Consult with an expert or peer group for unbiased input.

- Decide on clear metrics to track progress.

Skipping these steps all but guarantees misalignment between tool capabilities and real-world needs—a recipe for digital disillusionment.

Match the tool to the goal—not the hype

Each financial objective—saving for retirement, building an emergency fund, paying off debt—demands a tailored solution. The temptation to chase the latest trending app is powerful, but the optimal path means matching features, integrations, and usability to your unique context.

| Goal | Recommended tool types | Pros | Cons | Mobile compatibility |

|---|---|---|---|---|

| Budgeting | YNAB, Mint | Real-time tracking, alerts | Subscription fees, learning curve | Excellent |

| Investing | Betterment, Personal Capital | Automated, diversified | Limited customization | Good |

| Debt reduction | Tally, Undebt.it | Payment automation | Limited to certain debt types | Moderate |

| Tax optimization | TurboTax, Tax-Loss Harvesters | Integrated filing, advice | Privacy tradeoffs | Good |

| Charitable giving | Donor-advised funds (DAF) | Tax optimization, automation | Admin fees | Varies |

| Retirement planning | Wealthfront, Fidelity | Forecasting, goal tracking | May lack personal nuance | Excellent |

Table: Best-in-class tools by financial goal. Source: Original analysis based on Abacum, Moneywise, 2025

When Maya, a freelancer, switched from a generic app to a tool designed for irregular income, her savings rate doubled in six months. The differentiator? Features that fit her cash-flow reality, not the frictionless UI of the moment.

Build your plan, then automate—carefully

Automation is the holy grail of digital planning—recurring transfers, scheduled investments, automatic bill pay. But set-it-and-forget-it is a myth. According to industry experts, regular reviews are critical to catch drift, errors, or missed opportunities.

"Set it and forget it? Only if you like surprises." — Morgan (illustrative, based on security expert interviews)

The smart move: build your plan manually first, then layer on automation with tight guardrails. Schedule quarterly reviews, set up alerts for overdrafts or missed goals, and never turn off two-factor authentication. In the online world, vigilance is the price of freedom.

Case study: What happens when you go all-in online

Startup founder: from spreadsheets to AI dashboards

Elliot was a classic spreadsheet warrior, tracking both business and personal finances with endless tabs and late nights. The shift to AI-powered dashboards, triggered by rapid business growth, changed more than his workflow—it transformed outcomes. By deploying tools that integrated forecasting, tax optimization, and cashflow prediction, Elliot slashed administrative time by 60% and spotted a six-figure tax-saving opportunity missed by his accountant.

The irony? While automation did the heavy lifting, Elliot’s habit of reviewing dashboards weekly was what kept everything on track. The case for AI is strongest when paired with human discipline.

Family finances: turning chaos into clarity

The Alvarez family, multi-generational and multi-accounted, was drowning in paperwork and scattered statements. By consolidating everything through a unified online budgeting tool, they created a single source of financial truth. Automated bill pay ended late fees, goal-based savings brought transparency to family priorities, and access controls ensured privacy for sensitive accounts.

Less stress, more shared understanding, and a 30% improvement in household savings: the digital shift ended the “who paid what” arguments, replacing chaos with clarity. The lesson? Online tools amplify collaboration when set up with intention—not just convenience.

Freelancer hustle: maximizing every digital dollar

Freelancers face a uniquely brutal financial landscape—irregular income, unpredictable taxes, and no HR department for rescue. When Jamal adopted digital planning, he was skeptical. But the transformation was stark:

| Metric | Before (Manual) | After (Optimized) |

|---|---|---|

| Income volatility | High | Moderate |

| Savings rate | 5% | 18% |

| Tax prep time | 25 hours/year | 8 hours/year |

| Financial stress | Extreme | Low |

Table: Before and after: Freelancer financial outcomes. Source: Original analysis based on Moneywise, 2025; user stories

Jamal credits his success to frequent check-ins and not blindly trusting automation. His biggest mistake? Setting an auto-transfer too high and bouncing a rent check—an all-too-common digital pitfall.

The dark side: Security risks and privacy traps in online finance

How your data actually gets used (and misused)

Every digital platform—no matter how reputable—collects data. Account balances, spending patterns, investment choices, even physical location during logins. While most claim “bank-level” security, the reality is that data often flows to third-party analytics, marketing affiliates, and in some cases, insurance or lending arms hungry for insights.

According to recent research, over 70% of free financial apps share user data with at least one outside partner (Moneywise, 2025). The steps you can take: scrutinize privacy disclosures, opt out of marketing cookies, use encrypted connections, and periodically purge accounts you no longer use.

Red flags: What to watch for in online platforms

With new tools launching daily, not all platforms are created equal. Some are outright scams, others just poorly secured. Spotting a bad actor before damage is done is a non-negotiable skill.

- Red flags to watch out for in online financial platforms:

- Missing or vague privacy policies.

- No two-factor authentication.

- Poor app store reviews mentioning lost funds or support black holes.

- Excessive permissions requested on mobile.

- Lack of clear company ownership information.

- Guarantees of “risk-free” returns or outlandish performance claims.

- No visible regulatory compliance or insurance.

- Hidden fees buried in the terms of service.

To dig deeper, Google the company’s name with “complaint,” “breach,” or “scam.” Verify security credentials, look for FINRA/SEC registration for investment apps, and read independent reviews—not just star ratings.

Mitigating risk: Smarter security moves

Protecting your money online is about layers of defense. At a minimum, demand these security features from any tool you use:

| Security Feature | Description |

|---|---|

| Multi-factor auth (MFA) | Requires more than a password to log in |

| End-to-end encryption | Data is unreadable to third parties in transit |

| Transparent privacy policy | Explains who accesses your data and why |

| User reviews | Look for consistent positive experiences |

Table: Top security features to demand from financial apps. Source: Original analysis based on Moneywise, 2025

Regular audits—checking permissions, updating passwords, and closing unused accounts—matter more than ever. In the game of online finance, complacency is the biggest threat.

AI, automation, and the new rules of financial planning

What AI can do for you—and what it can’t

AI-powered financial planning tools are everywhere—promising to rebalance your portfolio, optimize taxes, and even anticipate “life events” from your spending. The technology is powerful: platforms like Abacum and Betterment use machine learning to offer highly personalized advice and enable fractional investing in alternative assets (Abacum, 2025).

But AI isn’t magic. It can’t read your mind, understand family dynamics, or factor in personal values the way a human can. It’s only as good as its data and programming—a fact proven by cases where algorithmic bias led to inappropriate portfolio recommendations or missed tax-advantaged opportunities.

The role of human judgment in a digital world

Intuition and lived experience are the ultimate counterweights to automation. Digital tools can spot patterns, but only you know your risk tolerance, values, and long-term priorities. The best outcomes come from blending AI suggestions with human oversight—reviewing recommendations, overriding when context demands, and questioning assumptions.

Overtrusting automation is the fastest way to get burned. As one financial planner told Financial Planning, 2025, “Good tools make you smarter; they don’t replace your brain.” When the stakes are high, use digital assistants as amplifiers—not substitutes—for your own judgment.

Emerging trends: What’s next for online finance

The pace of change in digital finance is relentless. New entrants, from legacy banks to crypto-native startups, are racing to add AI, gamification, and blockchain-based security to their platforms. Tokenization is breaking open access to private markets, and advanced tax optimization is now a mainstream feature.

Staying ahead means vigilance, curiosity, and a willingness to evolve. Resources like futuretoolkit.ai continue to track and synthesize the latest trends in business AI and online financial optimization, serving as a compass for those looking to future-proof their strategies in a fast-moving landscape. The winners will be those who adapt, learn, and experiment—always with eyes wide open to both opportunity and risk.

Beyond the basics: Advanced digital strategies for financial optimization

Cross-industry hacks you’re not using

Some of the best financial optimization strategies online are borrowed from beyond the finance world. Think like a supply-chain manager, marketer, or data scientist and you’ll find new ways to squeeze value from your digital stack.

- Unconventional uses for online financial planning tools:

- Use project management apps to plan debt payoff timelines.

- Apply marketing analytics techniques (like attribution modeling) to investment performance.

- Deploy customer relationship management (CRM) tools to track charitable giving and estate planning.

- Treat cashflow like inventory—forecast shortages and surpluses.

- Leverage A/B testing methods to optimize recurring expenses.

- Use business intelligence dashboards to visualize financial KPIs, not just sales.

By crossing boundaries, you gain an edge over those sticking to conventional finance-only tools.

Customizing your online toolkit for maximum impact

No single tool fits every user. The power lies in customization—building a stack that fits your goals, skills, and risk appetite.

- Step-by-step guide to building your online financial toolkit:

- Map out all financial needs (budgeting, investing, tax, philanthropy).

- Rate your comfort and skill level with technology.

- Research and shortlist tools for each need.

- Verify security and data policies for each tool.

- Test integrations (e.g., can your budgeting app pull investment data?).

- Set up automation with manual override options.

- Schedule quarterly reviews for updates and pruning.

The biggest pitfall? Chasing shiny features instead of real fit. Resist the urge to over-customize; simplicity and reliability always beat complexity.

Measuring success: What metrics really matter

The digital world loves vanity metrics—logins, “goals completed,” time spent. But real success comes from tracking outcomes that move the needle on your financial health.

Key performance indicators include savings rate, investment diversification, tax efficiency, and advice recall. When results don’t match expectations, use those metrics to course-correct—switch tools, adjust automation, or seek expert input.

Comparing the best: Online financial planning tools head-to-head

What sets the winners apart

The best online financial planning solutions distinguish themselves through seamless integration, robust automation, bulletproof security, and responsive support. Cost and mobile usability matter, but only when paired with features that serve real needs.

| Tool | Integration | Automation | Support | Cost | Mobile usability |

|---|---|---|---|---|---|

| Betterment | Excellent | Advanced | Good | $$ | High |

| Mint | Good | Basic | Moderate | Free | High |

| Abacum | Excellent | Moderate | Excellent | $$$ | Good |

| Personal Capital | Good | Good | Moderate | $$ | Good |

| YNAB | Moderate | Basic | Good | $$$ | Excellent |

Table: Online tool feature matrix. Source: Original analysis based on Abacum, Moneywise, 2025

Your priorities—cost, automation, support—should dictate your pick, not the flashiest marketing campaign.

Hidden dealbreakers: What reviews don’t tell you

User ratings are a starting point, not the end. Many reviews gloss over integration headaches, customer support bottlenecks, and limitations for non-standard income or family structures. Reading deep-dive forums or expert analyses reveals flaws that seldom make it into glossy testimonials.

The best defense is skepticism:

"Most reviews skip the ugly parts. Dig deeper." — Taylor (illustrative, based on consumer advocate interviews)

Testing yourself with a trial period, reading privacy policies, and verifying customer service response time can save months of regret.

How to decide: Personal, business, or hybrid?

Personal financial optimization tools focus on budgeting, investing, and retirement. Business tools layer in forecasting, multi-entity management, and regulatory compliance. Hybrid solutions—rising fast in 2025—combine both, serving freelancers, entrepreneurs, and families with complex needs.

Your ideal tool depends on organizational complexity, transaction volume, and the need to separate (or unify) personal and business finances. For small business owners, hybrid platforms offer control and oversight, but may demand steeper learning curves.

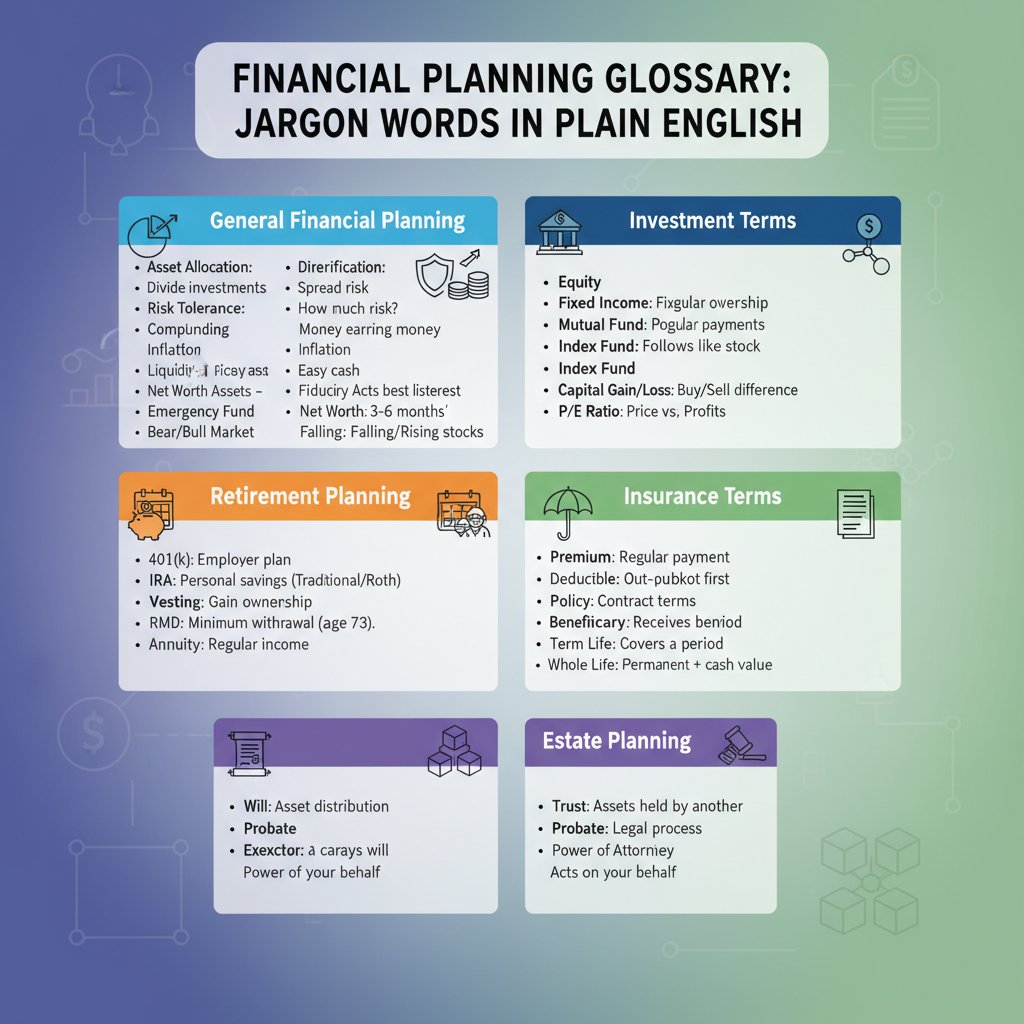

Glossary: Decoding online financial planning jargon

Key terms and what they really mean

An online platform that uses algorithms to manage investments automatically. Unlike a human advisor, it makes decisions based on your responses and market data, often at lower cost. Example: Betterment.

A tool that provides financial suggestions by learning from your data and behavior. Goes beyond automation by identifying patterns and offering personalized insights—think of it as your digital “second brain.”

Converting ownership of assets (like real estate) into digital “tokens” on a blockchain, allowing fractional investment and broader access.

Selling investments at a loss to offset taxes on gains. Done strategically by advanced platforms to optimize after-tax returns.

Buying a portion of a share, rather than a whole, to enable diversified investing without large capital outlay.

Misunderstanding these terms can lead to costly mistakes—downloading the wrong app, misunderstanding fees, or missing out on key features.

Common confusions: What’s the difference?

Many users confuse a robo-advisor with an AI assistant, or budgeting with cashflow management. The difference? Robo-advisors automate investing, while AI assistants offer broader, data-driven advice. Budgeting tracks spending; cashflow management forecasts and plans for future outflows and inflows.

Quick tip: Identify your need, then match to the right tool—don’t let buzzwords fool you. Clarity breeds confidence, and confident users get more from their tools.

Why language matters in digital finance

Words are weapons—and shields. Platforms that obfuscate with jargon or vague terminology often hide unclear fees, ambiguous data usage, or weak support. Demanding transparency in language is the first step to building trust.

When you see unclear terms, ask for clarification, search for independent definitions, and pressure providers to explain in plain English. Clear language builds confidence, cuts through hype, and leads to better outcomes.

Your next move: Taking action and staying ahead

How to build your own action plan

Mastery comes from action—not just reading. Consolidate your learnings into a practical, tailored plan.

- Action steps to optimize your financial planning online:

- Define your goals and constraints.

- Audit existing financial accounts and tools.

- Research and shortlist best-fit platforms.

- Set up robust security (MFA, strong passwords).

- Automate basic tasks, but review settings monthly.

- Track your progress with real KPIs.

- Review and adapt quarterly—never stand still.

A living plan beats a static one. Stay nimble, and course-correct as digital finance shifts.

Staying sharp: Avoiding digital complacency

The biggest risk is settling—assuming your current setup is “good enough.” Tools age, features lag, and new threats emerge. To keep your edge, make a habit of monitoring new solutions, attending webinars, and following resources like futuretoolkit.ai that analyze and curate AI-driven financial tools.

Digital vigilance means staying curious, questioning the status quo, and never abdicating judgment to an app—no matter how smart.

The bottom line: Your financial future, reimagined

Thriving in online financial planning isn’t about one killer app or secret hack. It’s a mindset shift: from passive consumer to active, informed operator. The brutal truth? Most online plans fail because users outsource thinking to tools, chase hype, or ignore security. The upside? Those who embrace skepticism, demand transparency, and blend automation with oversight stand to win—big.

So, take control. Tear down the myths, cut through the noise, and build a stack (and a playbook) that’s truly your own. The opportunity is real, but the traps are everywhere. Your move.

Sources

References cited in this article

- Financial Planning(financial-planning.com)

- Moneywise(moneywise.com)

- Abacum(abacum.ai)

- FPSB Value of Financial Planning Report 2023(fpsb.org)

- PYMNTS(pymnts.com)

- Financial Planning Association(financialplanningassociation.org)

- Kitces(kitces.com)

- Banque Havilland(banquehavilland.com)

- AI Advisory Group(aiadvisorygroup.com)

- Forrester(forrester.com)

- LinkedIn(linkedin.com)

- Wealth Solutions Report(wealthsolutionsreport.com)

- Frontdoor(frontdoor.com)

- American Planning Association(planning.org)

- Deloitte/ThinkNumbers(thinknumbers.com.au)

- EV UK(blog.ev.uk)

- HowFinanceTips(howfinancetips.com)

- MoneyFit(moneyfit.org)

- Forbes(forbes.com)

- Bankrate(bankrate.com)

- Centage(centage.com)

- Fortunly(fortunly.com)

- SkyQuest(skyquestt.com)

- Freelancermap(freelancermap.com)

- Forbes(forbes.com)

- Statista(statista.com)

- American Banker(americanbanker.com)

- Payments Intelligence(thepaymentsassociation.org)

- Strobes(strobes.co)

- CFO.com(cfo.com)

Ready to Empower Your Business?

Start leveraging AI tools designed for business success

Frequently Asked Questions

Why has financial planning shifted online?

Financial institutions moved to digital platforms due to convenience, cost-cutting measures, and technological advancement. COVID-19 accelerated this exodus from brick-and-mortar banking, forcing consumers from retirees to side hustlers to manage finances through apps and online dashboards.

What does the 2025 Moneywise study reveal about people's financial confidence online?

According to the study, 35% of U.S. adults expect to be better off financially in four years, but most report confusion and overwhelm with the available digital options, indicating that while digital access was democratized, clarity decreased.

What is the 'paradox of choice' in online financial planning?

The paradox of choice refers to the overwhelming number of options available—over 500 digital finance products on the U.S. market in 2025—which leaves consumers confused rather than empowered, despite having more access than ever before.

What promise did the shift to digital financial planning make, and did it deliver?

The shift promised democratized access, lower fees, and the ability to manage all finances independently without personal interaction. While it delivered access, reality showed too many tools with too little guidance, losing the personal touch that helped consumers navigate financial decisions.

Continue Reading

Keep exploring Comprehensive business AI toolkit

Rethink Your Finances: Are You Using the Wrong Tools?

Tools for streamlined financial planning has changed—discover the bold tools and secrets you need for real efficiency in 2026. Don’t settle for outdated advice.

9 Ways to Hack Financial Planning Before It Hacks You

Optimize financial planning quickly and easily with 9 unconventional strategies. Get ahead of the curve, ditch outdated advice, and transform your finances today.

Financial Planning Automation Tools That Pay Off (and When They Don’t)

Discover insights about financial planning automation tools

Are Your Financial Planning Tools Sabotaging You? the 2026 Reality

Tools to enhance financial planning accuracy are evolving fast—discover 11 edgy truths, hidden risks, and expert tips to get ahead in 2026. Don't let outdated habits cost you.

Are Your Financial Planning Tools Misleading You?

Tools for accurate financial planning just changed. Discover the 7 disruptive truths, hidden risks, and real-world solutions that redefine accuracy. Read before you decide.

Financial Budgeting Automation Tools That Backfire—And How to Win

Discover insights about financial budgeting automation tools

Automating Financial Planning Tasks in 2026: Wins, Risks, Reality

Discover insights about automating financial planning tasks

Would You Trust a Bot with Your Bottom Line?

Optimizing financial budgets automatically is transforming business. Discover the edgy realities, hidden risks, and actionable strategies for 2026 success.

Are You Brave Enough to Optimize Financial Planning Differently?

Optimize financial planning with proven strategies, real-world stories, and myth-busting insights for 2026. Get ahead, avoid pitfalls. Rethink your financial game now.

Is 'simple' the New Smart? Your Guide to Financial Planning Without Tech Headaches

Financial planning software without technical skills is finally possible. Discover how non-tech users are taking control with AI—and the traps to avoid. Read on.